Commercial real estate investment is one of the most structurally complex processes in the world of finance — and yet, beneath the surface of every deal, whether it’s a vacant strip center in Dearborn or a stabilized industrial building in Sterling Heights, lies the same fundamental anatomy.

Strip away the property type and price point, and the mechanics are remarkably consistent. Understanding how deals actually come together — step by step — is what separates investors who build lasting wealth from those who simply stay busy.

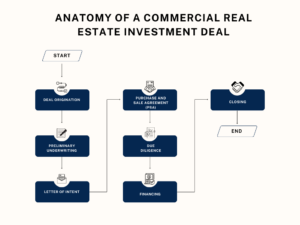

Deal Origination

Opportunities enter the pipeline through several channels: on-market listings, broker relationships, off-market seller outreach, and investor referral networks. The first filter is straightforward — does this property fit the investment thesis in terms of asset type, geography, price, and story? If yes, it moves forward. If not, disciplined investors pass without regret.

For those active in the Metro Detroit market, deal flow often hinges on broker relationships built over the years. Off-market deals in particular — properties never formally listed — are frequently the most attractively priced because sellers prioritize certainty and speed over exposure.

Preliminary Underwriting

Before scheduling a tour or submitting a letter of intent (LOI), buyers run a back-of-the-envelope stress test to determine whether the deal pencils at all. The key metric at this stage is the going-in cap rate: Net Operating Income (NOI) divided by purchase price.

In Metro Detroit today, that range spans considerably by asset class — from 5.5–6.5% for Class A multifamily to 9.5–12%+ for suburban office value-add plays. If the numbers don’t approach the investor’s required return threshold, the deal ends here. That’s not failure; that’s discipline. According to CBRE’s latest commercial real estate research, capitalization rates have been widening across multiple asset classes, making rigorous preliminary underwriting more critical than ever.

Letter of Intent (LOI)

The LOI is non-binding but structurally critical. It establishes the framework for price, earnest money, due diligence period length, financing contingencies, and closing timeline. A well-crafted LOI protects buyer flexibility while giving the seller enough confidence to take the property off the market.

Think of the LOI as the handshake before the contract. It telegraphs intent and professionalism, and in competitive situations — particularly in tight industrial corridors around Wayne and Oakland counties — the quality of the LOI itself can determine whether a seller chooses to negotiate with you at all.

Purchase and Sale Agreement (PSA)

Once the LOI terms are agreed upon, attorneys draft the binding Purchase and Sale Agreement (PSA), covering representations and warranties, conditions to close, escrow instructions, and default remedies. For investors deploying 1031 exchange proceeds — a powerful tax-deferral strategy under IRS Section 1031 — the PSA must explicitly account for assignment rights and the strict 45-day identification and 180-day closing windows that govern qualified exchanges.

Errors or omissions in the PSA can create significant exposure. Sophisticated investors ensure legal review is thorough, particularly on representations about environmental conditions, existing leases, and zoning compliance.

Due Diligence

Due diligence is where commercial real estate investment deals are won or lost. A standard 30–60 day period covers four parallel tracks:

- Physical: Property Condition Assessment (PCA), Phase I/II Environmental Site Assessment, mechanical and roof inspections.

- Financial: Rent roll verification, lease abstracts, trailing operating statements, and expense reconciliation.

- Legal: Title commitment review, survey, zoning confirmation, and tenant estoppel certificates.

- Market: Submarket vacancy, absorption trends, competitive rent analysis, demand drivers.

In Michigan’s industrial corridors — including the I-94 and I-75 corridors — environmental history deserves particular scrutiny given the region’s deep manufacturing heritage. The EPA’s environmental site assessment standards provide a clear framework for what Phase I and Phase II assessments must cover.

Experienced buyers use due diligence not just to confirm what they believe, but to find what the seller didn’t highlight. Every discovery is either a deal killer, a re-trade opportunity, or a data point that sharpens the underwriting.

Financing

Most commercial real estate investment deals involve leverage. With traditional bank lending constrained by CRE concentration limits — a concern highlighted repeatedly by the Federal Reserve’s banking supervision reports — private lenders and debt funds have filled the gap, often pricing transitional asset loans at 10–15%+ over benchmark rates.

Lenders run a parallel underwriting track alongside the buyer: ordering their own appraisal, reviewing the rent roll independently, and stress-testing Debt Service Coverage Ratio (DSCR) at various vacancy and interest rate scenarios. Timing the lender’s underwriting process to align with the PSA closing date is one of the most commonly overlooked logistical challenges in CRE transactions — and one of the most consequential when it goes wrong.

Closing

At closing, the title is finalized and insured, the funds are wired, the deed is recorded with the county, and property management is transferred. Even at this final stage, last-minute obstacles can derail a deal: lender conditions satisfied too late, title defects surfaced in the final commitment update, or appraisal shortfalls that create a financing gap.

The best commercial real estate brokers and investors don’t simply react to these risks — they anticipate them. Pre-closing checklists, proactive lender communication, and title company coordination are the unglamorous hallmarks of a smooth close.

The Bottom Line

A commercial real estate investment deal isn’t an event — it’s a process. Investors who understand the full anatomy of a deal make better decisions at every phase: they identify risk earlier, negotiate more effectively, and avoid costly surprises. Discipline in underwriting, thoroughness in due diligence, and clarity in deal structure are what separate investors who build lasting wealth from those who stay busy.

Whether you’re evaluating your first acquisition or your fiftieth, working with an experienced commercial real estate broker who knows the Metro Detroit and Southeast Michigan market can make the difference between a deal that closes and one that collapses at the finish line.

Ready to put this process to work?

Whether you’re a first-time commercial buyer or a seasoned investor looking to expand your portfolio in Southeast Michigan, our team is here to guide you through every phase of the deal — from identifying the right opportunity to navigating closing day. Contact me today to schedule a consultation.